Many people start prepping by buying various items that they read or hear about on the internet, they typically do this without any plan and end up with a bunch in of ‘prepp stuff’ and not useful resources, that can actually help them survive.

This ‘stuff’ is also typically not organized or stored properly and therefore when it’s needed it’s nowhere to be found and you are left scrambling, instead of executing your survival plan.

I believe, planning and organization are the keys to successful ‘prepping’, that is why I created the “PREPP LIST” (PL).

The PL is organized in a matrix format with various ‘Situational Prepp Kits’ along the top and the actual prepp ‘items’ listed down the side.

The ‘items’ are organized by prepp ‘Areas’ (Water, Food, Personal Care, Protection, Lighting, Tools, Community) and the prepp item ‘Function’ (For example in the ‘Water’ area the items are divided into three functions or purposes (Cleaning, Transferring and Storing).

Using this two level hierarchy for organization allows you to really understand what the purpose/function of each item is and it gives you insight on what ‘Areas’ you might be over or under prepared.

The use of ‘PREPP KITS’ (PK) allows you to plan what you will need based on the “situation” you are in, for example are you on foot far from home, or are you able to bugout with your camper /RV or better yet can you just bug-in.

Everyone’s “situations” are different, for me, living in Florida with a wife and toddler, my PKs are the following:

As you can see that ‘kits’ are organized in such as way where they “build on each other”, for example the ‘CAR BUGOUT KIT’ assumes that you also have the EDC BACKPACK, EMERGENCY PACK, BUGOUT BAG AND CAR CAMPING KIT, this way you do not have to have duplicate items in the various kits. Another way to think about them is like going from the “worst case scenario” all you have is your EDC, to “Best Case” that you are comfortably bugging in with all your preps.

There is also a Tab called “SINGLE PUROPOSE KITS” (SPK) these are (as the name suggests) kits that have one purpose or function, for example a “BLEED CONTROL KIT” only items that are for bleed control. Separating out these kits allows you to simplify the ‘PREPP LIST’, and helps you create actual ready ‘kits’ that you can just grab and go. As you begin to list out the various items on the PL you will notice items that ‘belong together’, and should be combined into a SPK.

Another thing I thought would be beneficial in the PL was a ‘NEED TO BUY’ column, this way you can not only list out the items you already own but also those you plan to purchase in the future.

Below is a link to my PL, feel free to download a copy and modify in anyway you see fit, if you think there are some items I’m missing please let me know, I’m always looking for ways to improve it.

Thanks

Here are a few live charts on the Russian economy.

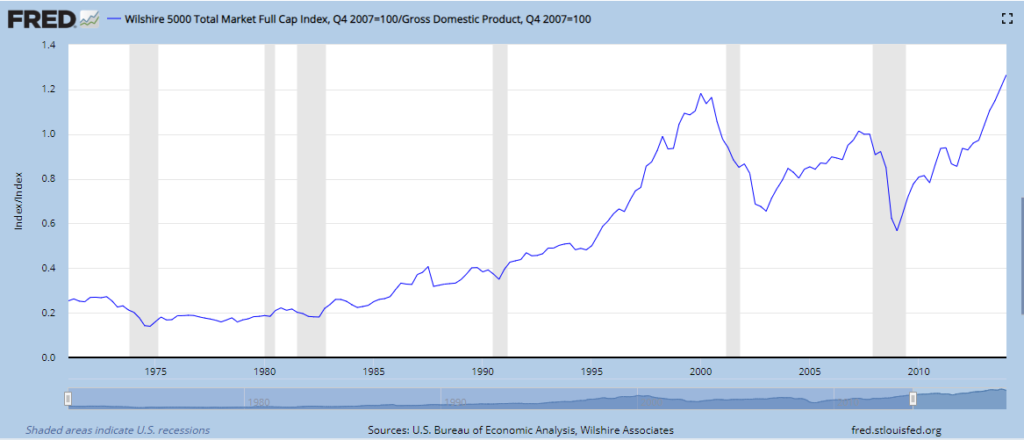

Owning Real Estate in Florida is not a bad idea as long as you know where the market is (in relationship to ‘Fair Value’) and you sell before the oceans rise.

As of Spring of 2019 I believe that we are ~20% over ‘Fair Value’ right now. My belief is based on inflation and population extrapolations. Population growth between 2000-2019 was ~23% and inflation of about ~49%. If you don’t believe that the dollar has lost almost half it’s buying power in the past 20 years, see for yourself https://smartasset.com/investing/inflation-calculator#LFWyzg1QVC

again make sure to sell before you’re (literally) under water…

STOCKS ARE OVER VALUED

THE ECONOMY IS NOT THAT GOOD

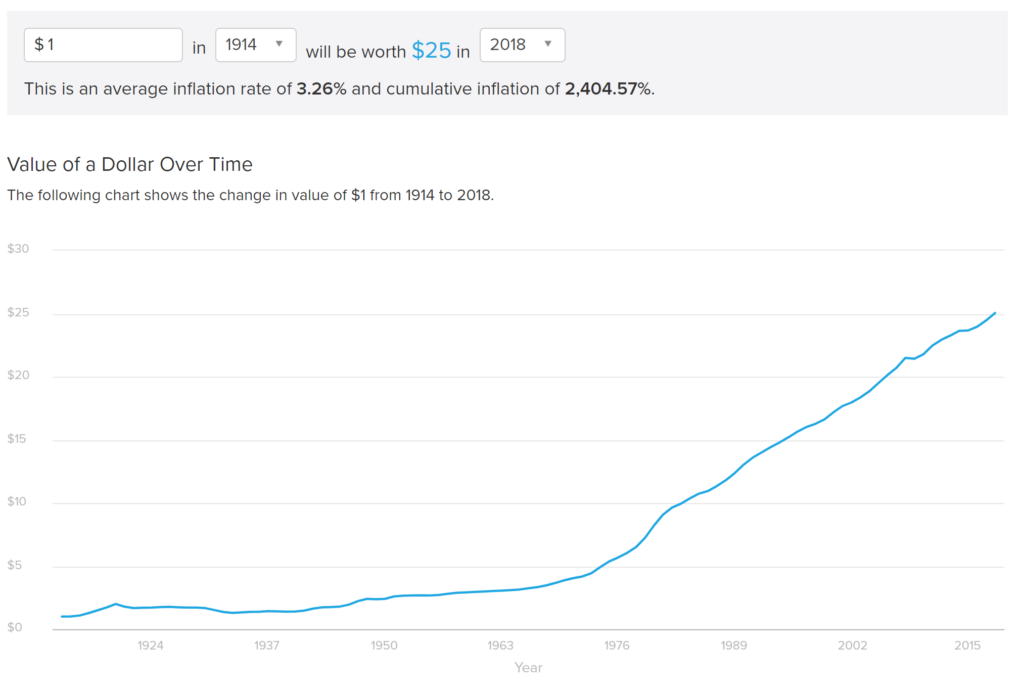

The US Federal Reserve dollar denominated notes, more commonly known as USD have actually been losing buying power since they were created in 1913. As you can see from this chart of USD inflation , $1 in 1913, had $25 worth of buying power by today’s metrics. For example you could buy $25 worth of groceries for just $1 in 1913. This also means that your $1 today is worth ~4% of it’s original value, said another way, the dollar has lost 96% of it’s original value (just imagine if a stock lost 96% of it’s value).

Also you can see from the chart that there was a significant change in the rate of growth of inflation in the early 70’s, that’s not accidental. In 1973 the US government completely came off the “gold standard” and would no longer require the USD to be backed with US Gold reserves. This officially turned the USD into a Fiat Currency, one that is not backed by any commodity (kind of like Bitcoin). Here is a video of Nixon “Temporarily” taking the US off the Gold Standard by suspending the convertibility of USD into Gold. Unfortunately this “Temporary” move became “Permanent”. and unlike Nixon hoped there is not an “overwhelming majority of Americans are buying American made products in America,” inflation effects buying power, that’s just a fact.

Now a few ‘notes’ on the US Federal Reserve (FED), as they are the ones in charge of USD ‘creation’ (inflation). Unlike what most people are brought to believe; the FED is not part of the US Federal Government, it’s a privet bank, run by other major privet banks, and USD is a “Bank Note” not a US government note. But don’t take my word for it, check out the FEDs own website. https://www.stlouisfed.org/in-plain-english/who-owns-the-federal-reserve-banks .

Just to put this into perspective, image another “branch” of the government, say the US armed forces, what if they were not part of the federal government and instead were a privet army operated by the major military contractors, (though through lobbying (legalized corruption) we have kind of reached a similar dynamic), but that’s a whole other story.

To be fair there is the ‘Board of Governors’ which are elected by the US presidents each for 14 Year term and they do have some say in what happens at the Fed. But a majority of them come directly from the banking industry or other questionable backgrounds which make you question who’s best interest they have in mind, is it the US public’s or someone else’s.

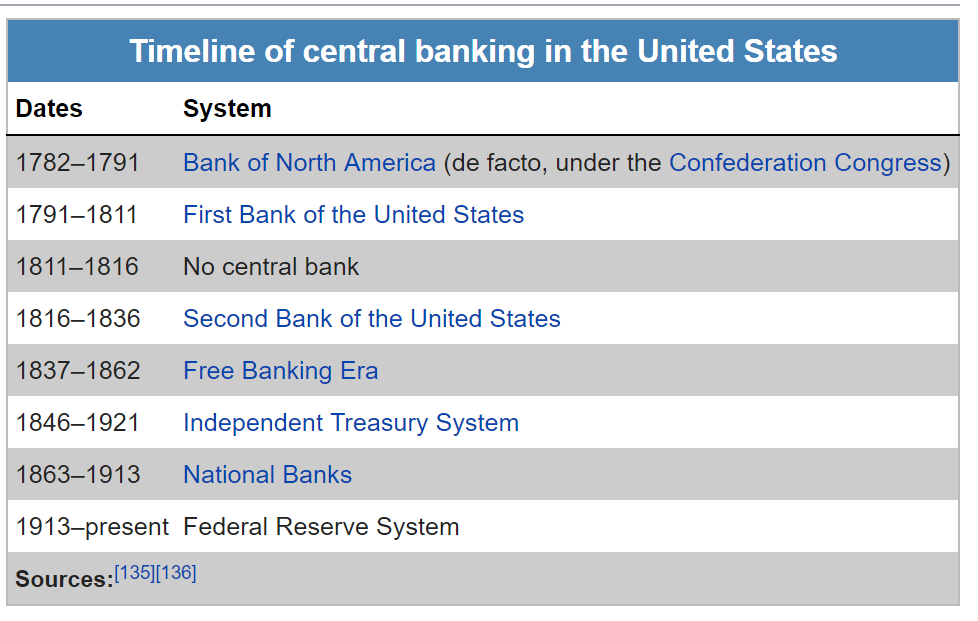

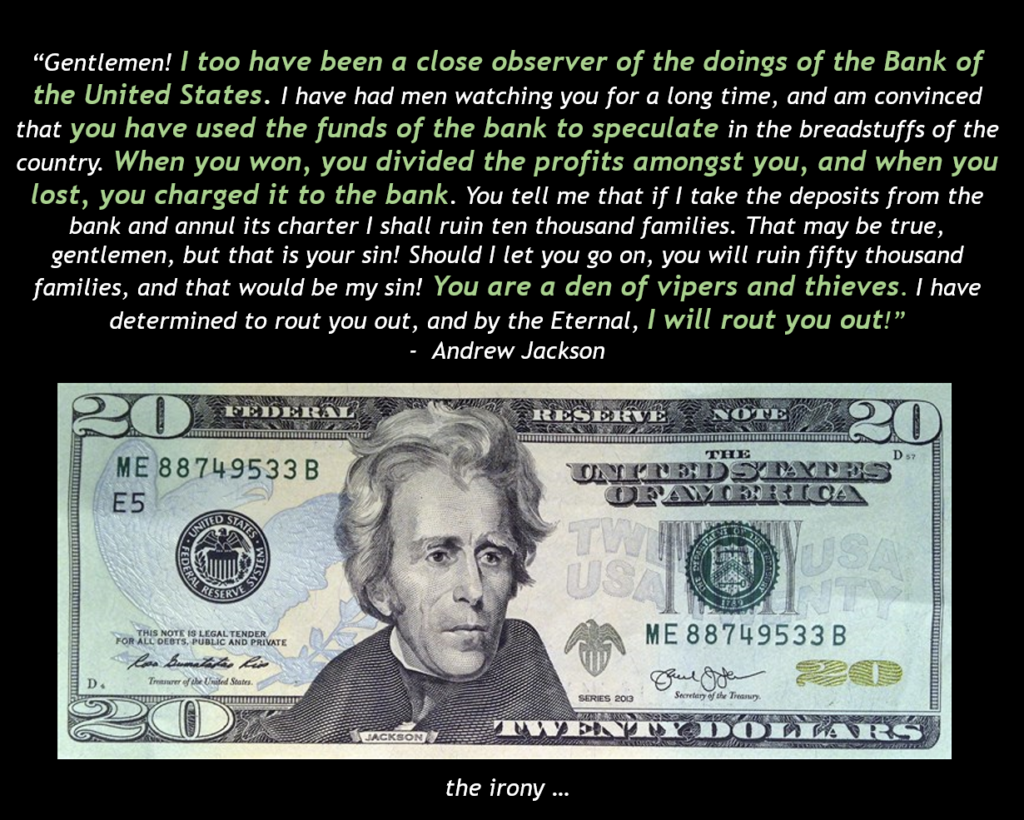

The US has actually been through several FEDs through-out its history, each one of them being abolished when their schemes become uncovered or unmanageable.

Here are just some choice words Andrew Jackson had for the FED of his time “Bank of US”, which he later helped abolish.

And if you didn’t think, having your nation’s currency run by an international banking syndicate was bad enough, let me tell you about ‘Fractional Reserve Banking’. As you probably know, banks don’t hold all their deposits, they lend them out , at interest, which makes sense as it’s highly unlikely that all the depositors will withdraw their funds at once. Therefor banks only have to hold the “minimum reserve requirement”. If you look at it a bit closer and do a few calculations you see something a bit odd, and even worrisome. With the current reserve rate of 10% (3% for banks that hold <$16M) a bank can create $1,000 out of $100. How? Well here is how it works: Once the bank receives $100 deposit is saves $10 and loans out the $90, the person with the $90, deposits it into the bank, (or pays some who deposits it into a bank), the bank keeps $9 and loans out $81, after this repeats 71 times, the banks have ‘created’ $900 out of thin air. Yes, the fractional reserve banking system has worked for many years, because as money is “created” when loans are made, it is “destroyed” when debts are payed back. But if the charts below are any indication, the later part of this equation is not happening as often as the the former.

As long as this trend persists, there is always new USD that is being added to the system, though as long as there is “Demand” for those additional dollars the inflation will not be significant, which has been the case for the last ~40 years.

So lets talk about “Demand”, which I think can be divided into two key sources, internal and external.

Internally as the US population increases so should the currency base, but as you can see the rate of population growth (~83% since 1960) is a bit lower than the increase in Money Supply (~600%).

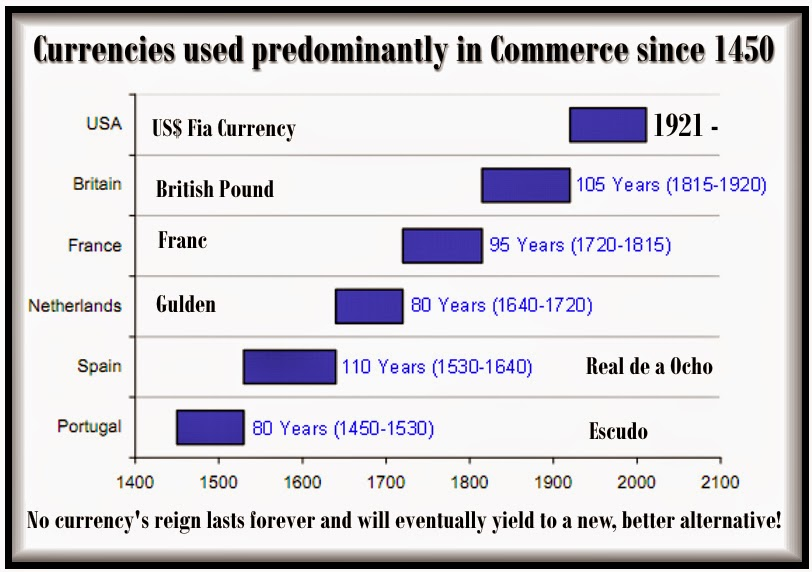

The FED (and US Government) has historically been able to manage inflation by increasing the global demand for USD. They have done this by offering high yield Treasury Bonds and crafting international trade agreements to require all parties to use USD. The ‘Petrodollar’ is a great example, in the early 70’s the US made several agreement with Saudi Arabia and OPEC to sell all their oil globally for USD, this meant that the US could print as much USD as there oil was being pumped out of the ground, as any country that wanted to buy oil would first need to ‘buy’ USD. Over the years these smart (but usually schemy) agreements have resulted in the USD becoming the world reserve currency, but as with all global reserve currencies in history, their time comes and goes, and as you can see from the chart below, they typically last ~100 years. Before the USD the British Pound was hailed as the global reserve currency as the British Empire was the dominant power of the 1800’s but as it’s military influence globally declined so did it’s currencies.

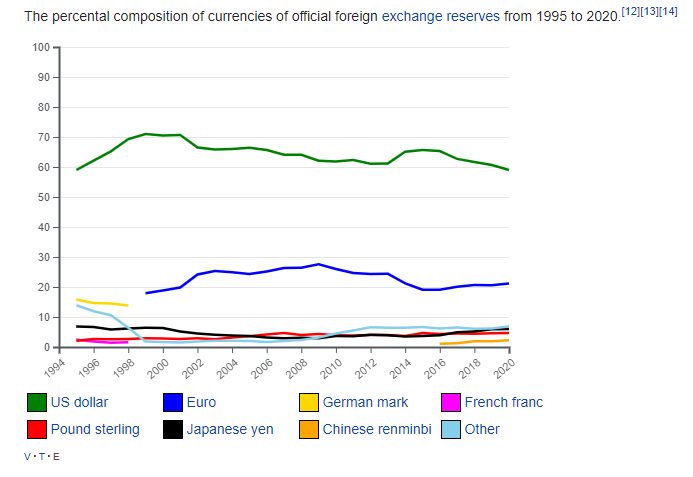

This is now happening to the US, as you can see from the chart below (from Wikipedia) though the USD is still the currency held the most by foreign countries, it’s role is declining, unlike the exponentially increasing debt (and therefore circulating USD).

There are a few key factors that I believe will impact the already falling global demand for USD. First is the emergence of new global powers like China and India and a general move away from relying on the US as the one world “Super Power”. Geopolitical events and policies such as sanctions, have also lead to more and more countries moving away from the dollar for conducting trade. Cryptocurrency, like Bitcoin, are beginning to make it possible to send money globally instantly on a ‘trust-less’ system, which would take the role the USD takes in global trade. Granted with the current price volatility and low market cap/liquidity of Cryptocurrency, it make it difficult to use it large scale international trade settlement, but as more and more institutional investors get into Cryptocurrency, the market will stabilize, and become used more and more for transactions instead of speculation.

As the rest of the world begins to reduce it’s USD holdings (typically held in the form of US Treasuries) the FED is continuing to buy them up. Though this has worked for Japan who’s central bank owns over 70% of the countries national debt, it’s not clear how this would work for a reserve currency, at some point people will begin to catch on to this being literal Debt Monetization or Government printing and spending money out of thin air.

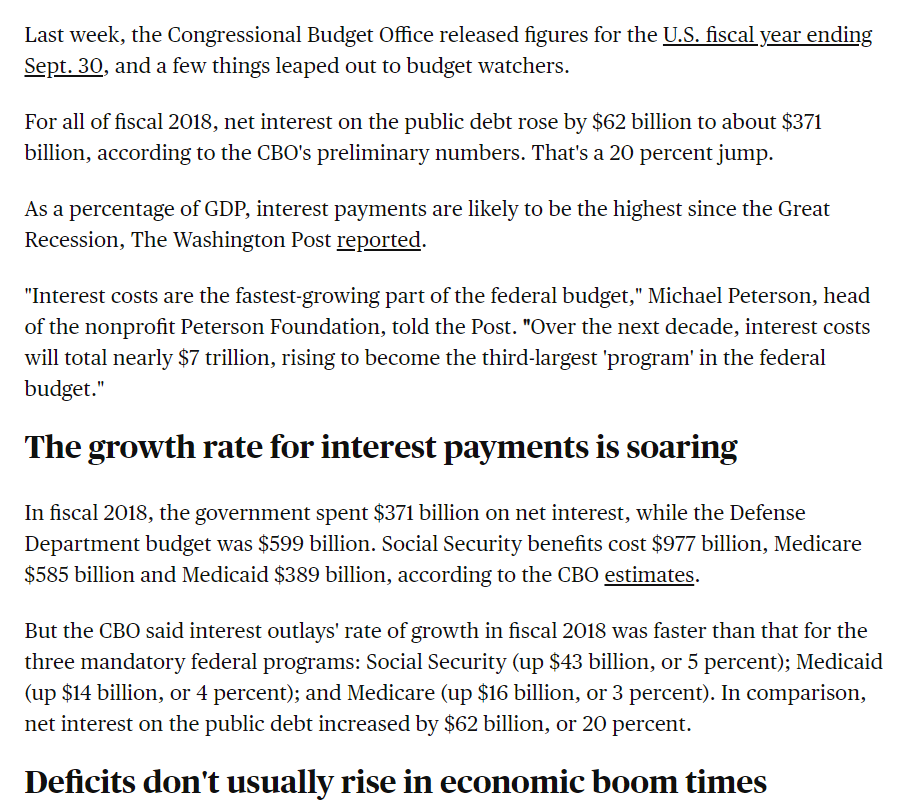

But the biggest factor that I think will contribute to the collapse of the USD ‘value’, is US government debt. As you can see from the chart above the the US has passed the mark of 100% Debt to GDP, for the first time since WW2. The debt itself is not an issue, it can hypothetically rise for ever, but the interest payments are another story.

At the time of this (initial) writing the US Debt is was~$22 Trillion (you can see a live debt “clock” on right sidebar), with interest rates at near zero the past 10 years, paying the interest has not been an issue. Though it still account for more than half of the US military spending (which as you know is the largest in the world). As you can see from the chart below the interest rate has been to almost 20% in the past, but lets assume we just get back to the average ~5%, that mean the US government will have to pay over $1 Trillion, that would be +25% of the 2018 US budget going to just pay interest!

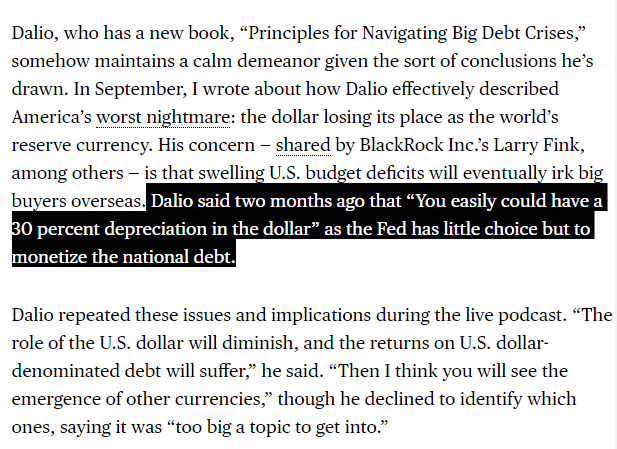

As you can see in the chart above of the Dollar Index (DXY) though it has gone through several ‘cycles’ there is a pattern forming of ‘lower highs’ and ‘lower lows’. This makes me believe that Ray Dalio’s prediction that the USD will lose ~30% of it’s value in the next downturn, is not too far fetched.

So what do you want to own, an asset that has been valued for thousands of years, or paper.

So now you’re probably wondering, how do I get my hands on some silver?

As with most purchased these days, you have two main options, online or in-person retail. The advantages of each are about the same as with choosing to buy a TV on Amazon or at Best Buy. Online is (almost) always cheaper and you will have a much bigger selection, but by buying something in person, you get the added benefit of taking your silver home with you that day and the comfort of knowing that if you have any questions (or issues) regarding your purchase you have someone to speak with (or confront).

If you want to invest in physical silver, In my opinion, you have three major categories of silver to choose from; Nationally Minted Silver (NMS), Privately Minted Silver (PMS) or Manufactured Silver Goods, such as jewelry and Silverware. In this post I’ll discuss what I see as the benefits and drawbacks of each one of these options, and which you should put your paper money in.