As of this writing (March 2019) stocks are beginning to come off their historic all time highs, could they recover and go higher? Yes, but is that a risk worth taking, I don’t think so.

The key to investing (in anything) is ‘Buy Low’ and ‘Sell High’, yes, it’s that simple. The only question is, what is ‘Low’ and what is ‘High’? Unfortunately there is no simple (or single) answer to this question, it’s all in who you ask.

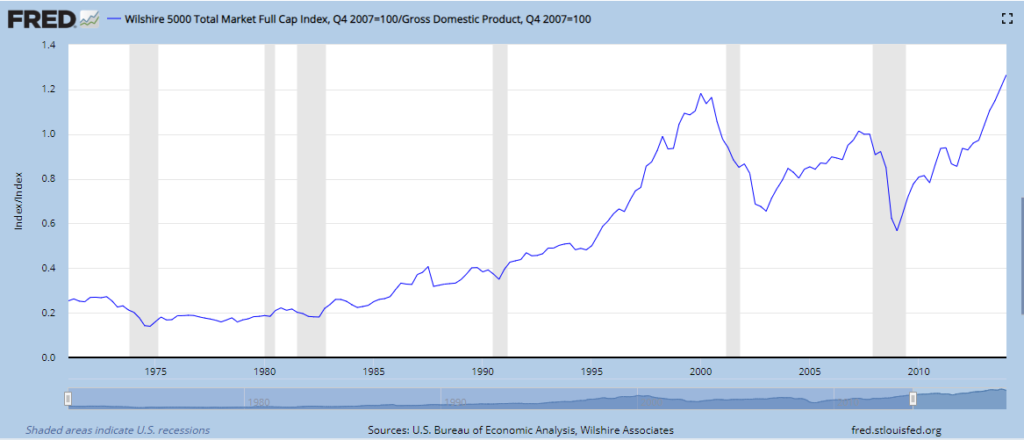

One person to ask might be Warren Buffet, fortunately he has already told us. If you take the total value of all issued stock in a country and divide it by the countries total annual production get an indicator called, Market Cap /GDP. Which Buffet stated “is probably the best single measure of where valuations stand at any given moment.” This is similar to a PE (Price to Earnings) ratio for a company, but you are looking at the countries economy as a whole.

The indicator below is typically used to shows how ‘inline’ stock prices are compared to the overall US economic output. As you can see we are currently above the levels we were, right before the dot com bubble bust in early 2000, a time when companies who had a domain name were worth millions, until they weren’t.

There are many people, primarily in the media, saying that the economy is great because employment in the US is doing great. The reason they say this is because the US “Unemployment Rate” is at all time lows, but I want to show you how the ‘Unemployment Rate’ and ‘Actual Employment’ are not as closely related, as you might think.

Below are a few charts I pulled from FRED, an economic data resource provided by the Federal Reserve. For starters only ~60% of the US population is actually working, well I guess there could be a bunch of children and retirees, who rightfully should not be in the workforce.

The title of the is chart is very misleading (source)

– INFLATION

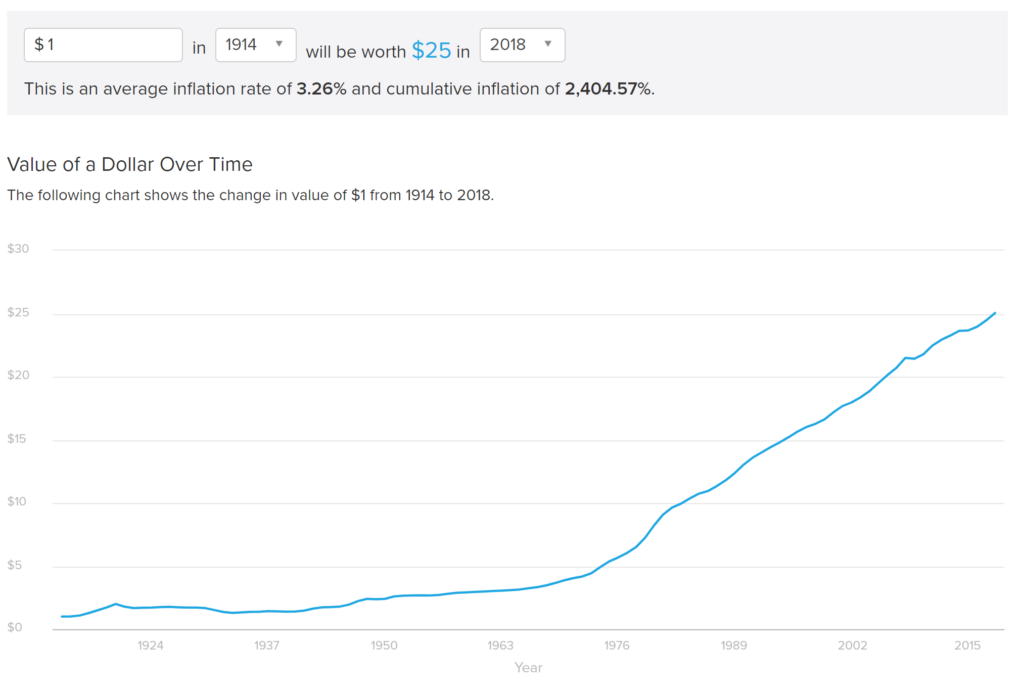

The US Federal Reserve dollar denominated notes, more commonly known as USD have actually been losing buying power since they were created in 1913. As you can see from this chart of USD inflation , $1 in 1913, had $25 worth of buying power by today’s metrics. For example you could buy $25 worth of groceries for just $1 in 1913. This also means that your $1 today is worth ~4% of it’s original value, said another way, the dollar has lost 96% of it’s original value (just imagine if a stock lost 96% of it’s value).

Also you can see from the chart that there was a significant change in the rate of growth of inflation in the early 70’s, that’s not accidental. In 1973 the US government completely came off the “gold standard” and would no longer require the USD to be backed with US Gold reserves. This officially turned the USD into a Fiat Currency, one that is not backed by any commodity (kind of like Bitcoin). Here is a video of Nixon “Temporarily” taking the US off the Gold Standard by suspending the convertibility of USD into Gold. Unfortunately this “Temporary” move became “Permanent”. and unlike Nixon hoped there is not an “overwhelming majority of Americans are buying American made products in America,” inflation effects buying power, that’s just a fact.

CAUSED BY THE FED

Now a few ‘notes’ on the US Federal Reserve (FED), as they are the ones in charge of USD ‘creation’ (inflation). Unlike what most people are brought to believe; the FED is not part of the US Federal Government, it’s a privet bank, run by other major privet banks, and USD is a “Bank Note” not a US government note. But don’t take my word for it, check out the FEDs own website. https://www.stlouisfed.org/in-plain-english/who-owns-the-federal-reserve-banks .

Just to put this into perspective, image another “branch” of the government, say the US armed forces, what if they were not part of the federal government and instead were a privet army operated by the major military contractors, (though through lobbying (legalized corruption) we have kind of reached a similar dynamic), but that’s a whole other story.

To be fair there is the ‘Board of Governors’ which are elected by the US presidents each for 14 Year term and they do have some say in what happens at the Fed. But a majority of them come directly from the banking industry or other questionable backgrounds which make you question who’s best interest they have in mind, is it the US public’s or someone else’s.

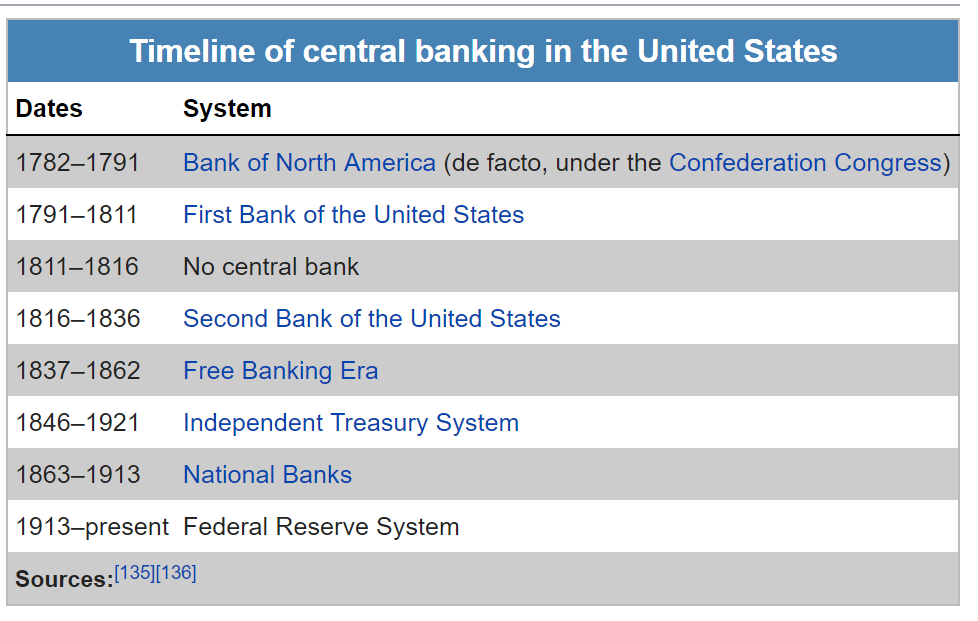

The US has actually been through several FEDs through-out its history, each one of them being abolished when their schemes become uncovered or unmanageable.

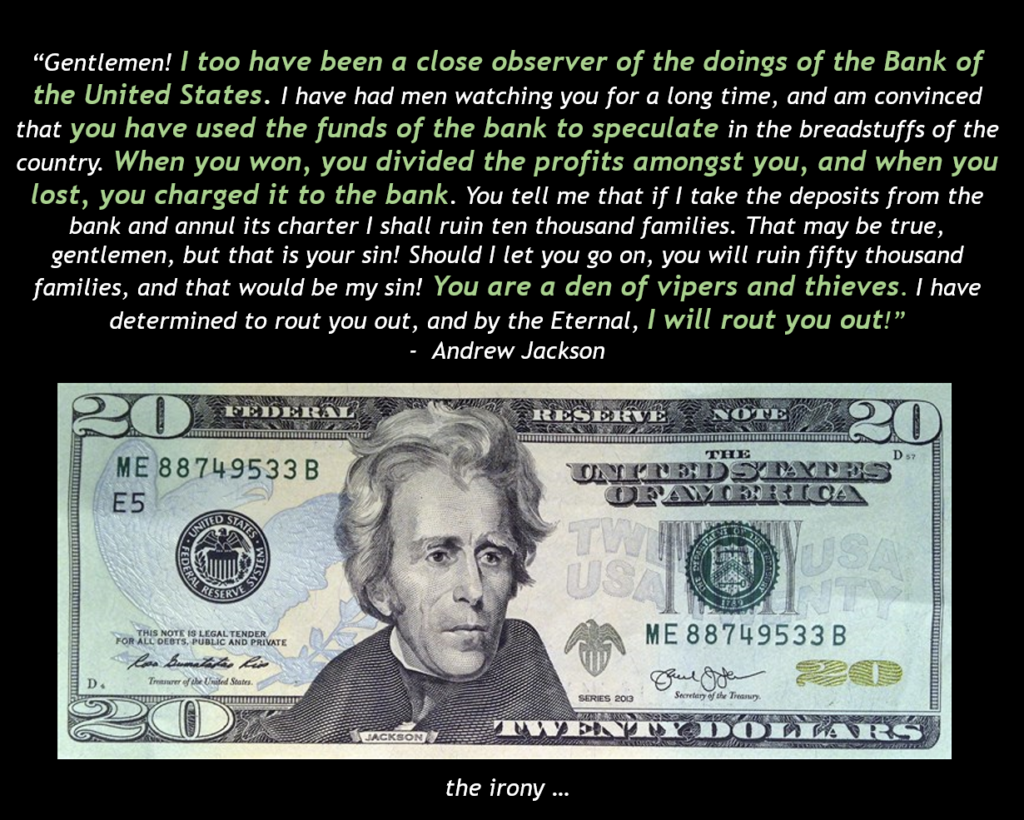

Here are just some choice words Andrew Jackson had for the FED of his time “Bank of US”, which he later helped abolish.

After Jackson abolished the “Bank of US” the US government actually had control of it’s currency for almost 100 years. The irony that the current central (privet) bank put him on thier most popular “note”, can be appreciated. (source)

& FRACTIONAL RESERVE BANKING

And if you didn’t think, having your nation’s currency run by an international banking syndicate was bad enough, let me tell you about ‘Fractional Reserve Banking’. As you probably know, banks don’t hold all their deposits, they lend them out , at interest, which makes sense as it’s highly unlikely that all the depositors will withdraw their funds at once. Therefor banks only have to hold the “minimum reserve requirement”. If you look at it a bit closer and do a few calculations you see something a bit odd, and even worrisome. With the current reserve rate of 10% (3% for banks that hold <$16M) a bank can create $1,000 out of $100. How? Well here is how it works: Once the bank receives $100 deposit is saves $10 and loans out the $90, the person with the $90, deposits it into the bank, (or pays some who deposits it into a bank), the bank keeps $9 and loans out $81, after this repeats 71 times, the banks have ‘created’ $900 out of thin air. Yes, the fractional reserve banking system has worked for many years, because as money is “created” when loans are made, it is “destroyed” when debts are payed back. But if the charts below are any indication, the later part of this equation is not happening as often as the the former.

As long as this trend persists, there is always new USD that is being added to the system, though as long as there is “Demand” for those additional dollars the inflation will not be significant, which has been the case for the last ~40 years.

FALLING DEMAND

So lets talk about “Demand”, which I think can be divided into two key sources, internal and external.

Internally as the US population increases so should the currency base, but as you can see the rate of population growth (~83% since 1960) is a bit lower than the increase in Money Supply (~600%).

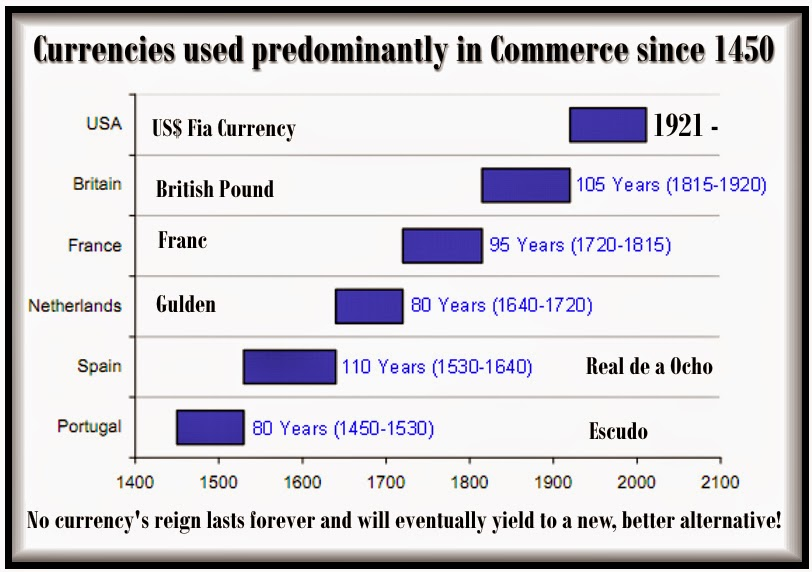

The FED (and US Government) has historically been able to manage inflation by increasing the global demand for USD. They have done this by offering high yield Treasury Bonds and crafting international trade agreements to require all parties to use USD. The ‘Petrodollar’ is a great example, in the early 70’s the US made several agreement with Saudi Arabia and OPEC to sell all their oil globally for USD, this meant that the US could print as much USD as there oil was being pumped out of the ground, as any country that wanted to buy oil would first need to ‘buy’ USD. Over the years these smart (but usually schemy) agreements have resulted in the USD becoming the world reserve currency, but as with all global reserve currencies in history, their time comes and goes, and as you can see from the chart below, they typically last ~100 years. Before the USD the British Pound was hailed as the global reserve currency as the British Empire was the dominant power of the 1800’s but as it’s military influence globally declined so did it’s currencies.

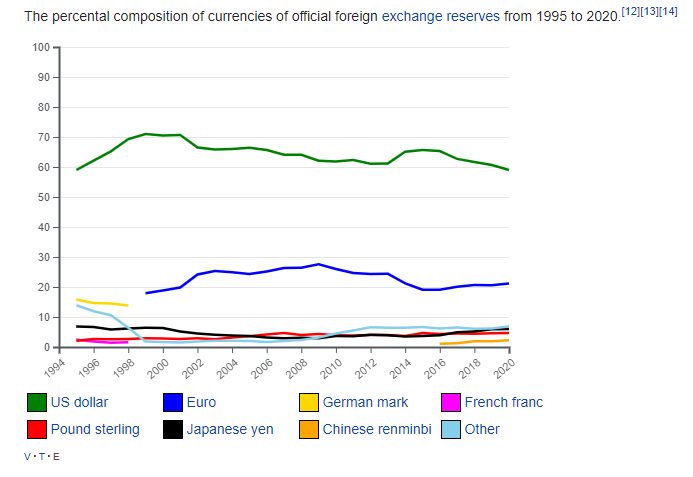

This is now happening to the US, as you can see from the chart below (from Wikipedia) though the USD is still the currency held the most by foreign countries, it’s role is declining, unlike the exponentially increasing debt (and therefore circulating USD).

There are a few key factors that I believe will impact the already falling global demand for USD. First is the emergence of new global powers like China and India and a general move away from relying on the US as the one world “Super Power”. Geopolitical events and policies such as sanctions, have also lead to more and more countries moving away from the dollar for conducting trade. Cryptocurrency, like Bitcoin, are beginning to make it possible to send money globally instantly on a ‘trust-less’ system, which would take the role the USD takes in global trade. Granted with the current price volatility and low market cap/liquidity of Cryptocurrency, it make it difficult to use it large scale international trade settlement, but as more and more institutional investors get into Cryptocurrency, the market will stabilize, and become used more and more for transactions instead of speculation.

As the rest of the world begins to reduce it’s USD holdings (typically held in the form of US Treasuries) the FED is continuing to buy them up. Though this has worked for Japan who’s central bank owns over 70% of the countries national debt, it’s not clear how this would work for a reserve currency, at some point people will begin to catch on to this being literal Debt Monetization or Government printing and spending money out of thin air.

& THE EVER-INCREASING US DEBT

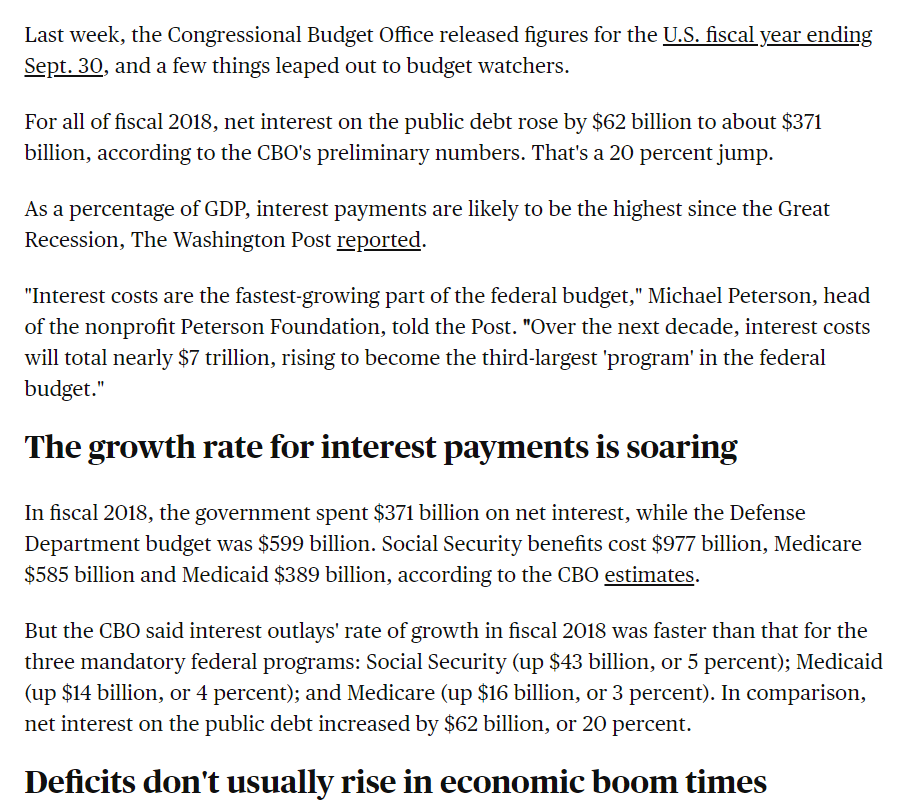

But the biggest factor that I think will contribute to the collapse of the USD ‘value’, is US government debt. As you can see from the chart above the the US has passed the mark of 100% Debt to GDP, for the first time since WW2. The debt itself is not an issue, it can hypothetically rise for ever, but the interest payments are another story.

At the time of this (initial) writing the US Debt is was~$22 Trillion (you can see a live debt “clock” on right sidebar), with interest rates at near zero the past 10 years, paying the interest has not been an issue. Though it still account for more than half of the US military spending (which as you know is the largest in the world). As you can see from the chart below the interest rate has been to almost 20% in the past, but lets assume we just get back to the average ~5%, that mean the US government will have to pay over $1 Trillion, that would be +25% of the 2018 US budget going to just pay interest!

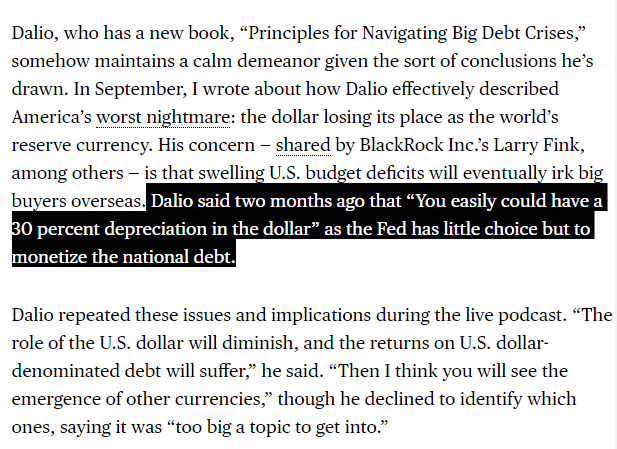

As you can see in the chart above of the Dollar Index (DXY) though it has gone through several ‘cycles’ there is a pattern forming of ‘lower highs’ and ‘lower lows’. This makes me believe that Ray Dalio’s prediction that the USD will lose ~30% of it’s value in the next downturn, is not too far fetched.

So now you’re probably wondering, how do I get my hands on some silver?

As with most purchased these days, you have two main options, online or in-person retail. The advantages of each are about the same as with choosing to buy a TV on Amazon or at Best Buy. Online is (almost) always cheaper and you will have a much bigger selection, but by buying something in person, you get the added benefit of taking your silver home with you that day and the comfort of knowing that if you have any questions (or issues) regarding your purchase you have someone to speak with (or confront).

If you want to invest in physical silver, In my opinion, you have three major categories of silver to choose from; Nationally Minted Silver (NMS), Privately Minted Silver (PMS) or Manufactured Silver Goods, such as jewelry and Silverware. In this post I’ll discuss what I see as the benefits and drawbacks of each one of these options, and which you should put your paper money in.

Silver price is massively under valued due to the price manipulation preformed by banks since the late 1800’s. If we revert back to the historic (300+ yrs) Gold/Silver price ratio, silver should we worth ~$80/oz. at today’s gold price of ~$1,300/oz. (which many believe is itself undervalued)