STOCKS ARE OVER VALUED

- As of this writing (March 2019) stocks are beginning to come off their historic all time highs, could they recover and go higher? Yes, but is that a risk worth taking, I don’t think so.

- The key to investing (in anything) is ‘Buy Low’ and ‘Sell High’, yes, it’s that simple. The only question is, what is ‘Low’ and what is ‘High’? Unfortunately there is no simple (or single) answer to this question, it’s all in who you ask.

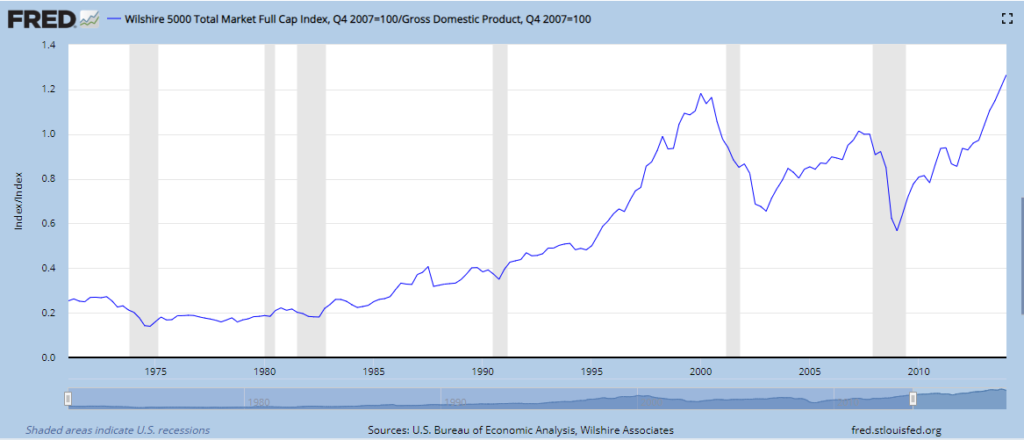

- One person to ask might be Warren Buffet, fortunately he has already told us. If you take the total value of all issued stock in a country and divide it by the countries total annual production get an indicator called, Market Cap /GDP. Which Buffet stated “is probably the best single measure of where valuations stand at any given moment.” This is similar to a PE (Price to Earnings) ratio for a company, but you are looking at the countries economy as a whole.

- The indicator below is typically used to shows how ‘inline’ stock prices are compared to the overall US economic output. As you can see we are currently above the levels we were, right before the dot com bubble bust in early 2000, a time when companies who had a domain name were worth millions, until they weren’t.

- If you want more information on the ‘Buffet Indicator’, check out https://www.gurufocus.com/stock-market-valuations.php.

THE ECONOMY IS NOT THAT GOOD

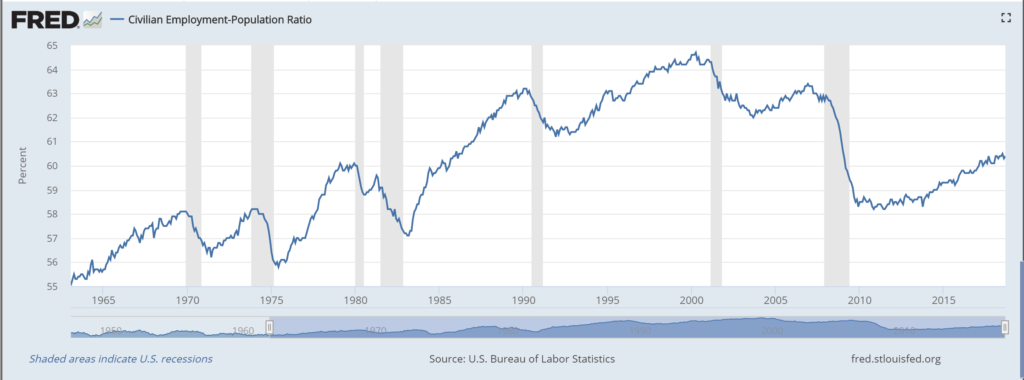

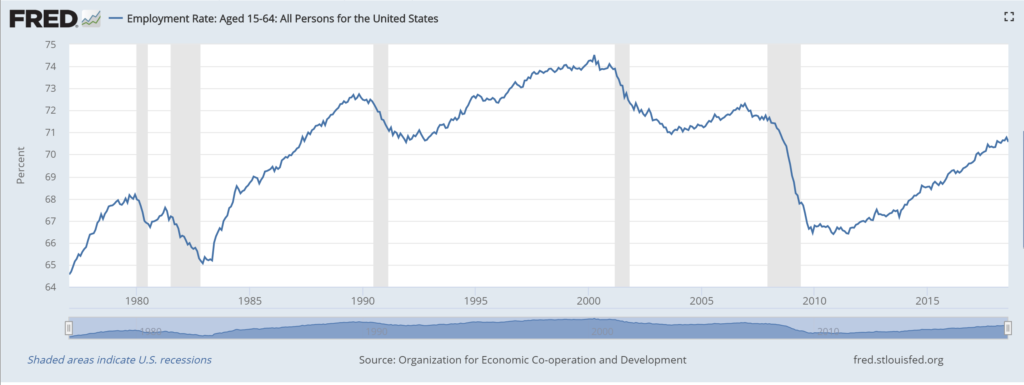

- There are many people, primarily in the media, saying that the economy is great because employment in the US is doing great. The reason they say this is because the US “Unemployment Rate” is at all time lows, but I want to show you how the ‘Unemployment Rate’ and ‘Actual Employment’ are not as closely related, as you might think.

- Below are a few charts I pulled from FRED, an economic data resource provided by the Federal Reserve. For starters only ~60% of the US population is actually working, well I guess there could be a bunch of children and retirees, who rightfully should not be in the workforce.

- Ok, taking out kids (Under 15) and old people (over 64) we are still left with only 70% employment, well what about collage students and maybe some people retire early?

- Even taking those out you are still left with less than 80% of this countries population being employed. 1 out of ever 5 Americans in their prime working age (25-54) does not have a job, today in the age of ‘3.75% Unemployment’. How does that make any sense?

- Though even looking at the ‘adjusted’ unemployment rate that is being reported on the main street media you can see an interesting pattern emerge, each time unemployment rate gets lower than 4-5% or there is trend bottoming we see a recession in the near future.

- Another interesting thing to notice is how the ‘unemployment rate’ is lower now than it was in 2000, though as you can see from the previous chart that the percentage employed of each category peaked right before the 2000 dot com bubble bust and has never recovered. This has a lot to do with retiring Baby-Boomers, whose open positions are now disappearing due to automation or globalization.

- If you want to learn more about the manipulation of government economic statistics, check out http://www.shadowstats.com/

BONDS WONT SAVE YOU

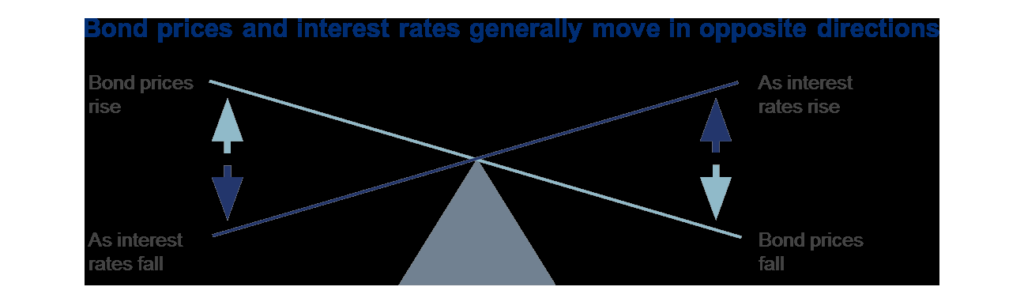

- Many people believe that if Stocks are predicted to go down, then Bonds will go up. While in typical market cycles this is true, due to the fact that in times of financial stress, the FED will lower interest rates, allowing people to borrow their way out of their financial problems or at least not crash the system. The rate drop means that bonds issued in the past with a higher interest rate will be worth more than the bonds being issues now that have a lower rate, this has been true for the last ~30 yrs. On the other hand as rates rise, previously issued, bonds (with set lower rates) will sell at a discount (on secondary markets) as the newly issued bonds will return more due to the higher interest rate.

- Since the 2008 Financial Crisis, the US FED funds rate has been near zero, you can’t get much lower. In the past few years the FED has been trying to raise rates, but stopped at 2.5% after the stock market had a near heart attack in December of 2018. Yes, they can drop rates 2.5% or if they want to take to the next level, they could go to negative rates, like they have in Japan and EU. But this can only go on until inflation starts creeping, people will stop holding the dollar, why would they, if they can instead hold something increasing in value, the FED will have to raise rates, therefore bond prices will have to go down. In the near term, while the FED is ‘responding’ to the coming market downtown, holding quality bonds might now be a bad idea. But long term, and this might be sooner than later, they FED will start raising rates, at the expense of the economy, to save the dollar from the inflation we talked about in the previous post.

- If you want tolearn more about bonds, check out http://funds.rbcgam.com/learning-centre/investing-basics/fixed-income-investing.html

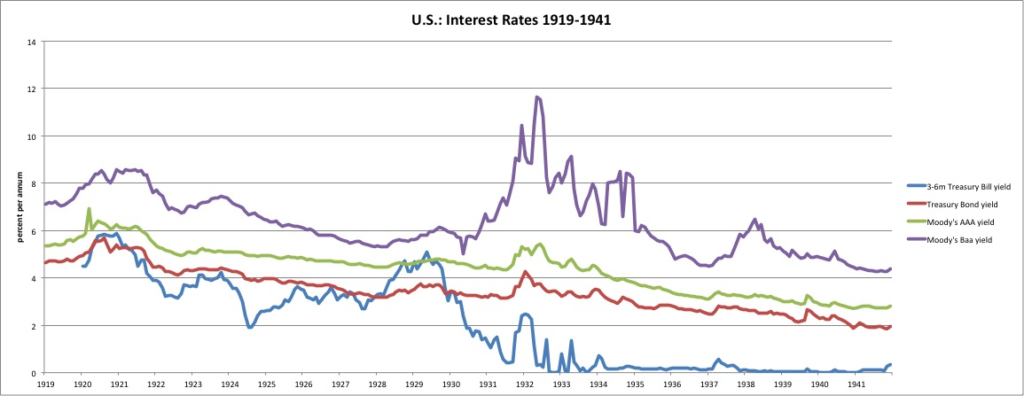

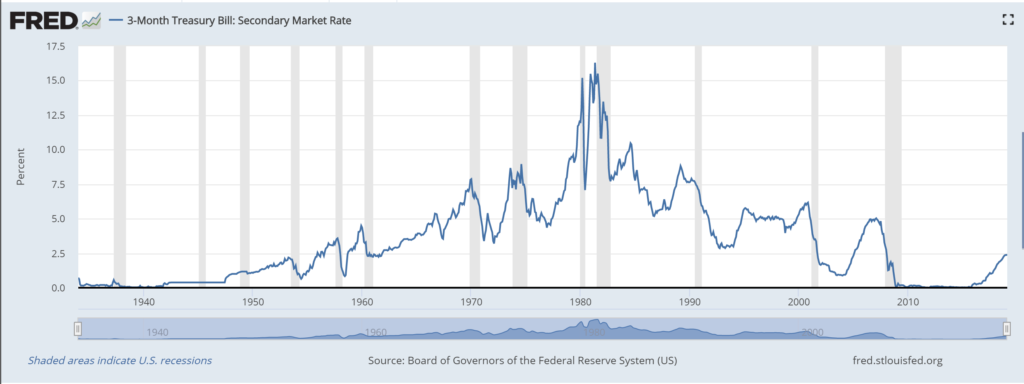

- Below are few charts showing the Historic interest rates, do you notice the cyclical pattern? Going down, coming up, going down, and now beginning to come back up.

- This is scary because as is stated earlier, most people have the false sense of security thinking that Stocks and Bonds “Always” move in opposite directions, therefore by holding both you have a ‘safe’ or hedged portfolio, while this is true in the smaller cycles, this is not the case in the larger cycle, a new leg of which i believe we are beginning. That is why I believe acquiring and holding physical assets (Gold, Silver, Real Estate) is the most secure thing to do in today’s markets.